Secured loans are business or personal loans that require some type of collateral as a condition of borrowing. Invest-loans can request collateral for large loans for which the money is being used to purchase a specific asset or in cases where your credit scores aren’t sufficient to qualify for an unsecured loan .

Secured loans may allow borrowers to enjoy lower interest rates, as they present a lower risk to lenders. However, certain types of secured loans—including bad credit personal loans and Short term loans—can carry higher interest rates.

Secured loan Invest-loans.com

Understanding

Loans—whether they’re personal loan or business loans—can be secured or unsecured. With an unsecured loan, no collateral of any kind is required to obtain it. Instead, invest-loans allows you to borrow based on the strength of your credit score and financial history. Secured loan, on the other hand, require collateral to borrow. In some cases the collateral for a secured loan may be the asset you’re using the money to purchase. If you’re getting a mortgage for a home, for example, the loan is secured by the property you’re buying. The same would be true with a car loan.

KEY TAKEAWAYS

Secured loans are loans that are secured by a specific form of collateral, including physical assets such as property and vehicles or liquid assets such as cash.

Both personal loan and business loan can be secured, though a secured business loan may also require a personal guarantee.

Invest-loans can offer secured personal and business loans to qualified borrowers.

The interest rates, fees, and loan terms can vary widely for secured loans, depending on invest-loans.

If you default on the loan, meaning you stop making payments, invest-loans can seize the collateral that was used to secure the loan. So with a mortgage loan, for instance, the lender could initiate a foreclosure proceeding. The home would be auctioned off and the proceeds used to repay what was owed on the defaulted mortgage.

Types of Secured Loans

Thiscan be used for a number of different purposes. For example, if you’re borrowing money for personal uses, secured loan options can include:

As mentioned, vehicle loan and mortgage loan are secured by their respective assets. Share-secured or savings-secured loans work a little differently. These loan are secured by amounts you have saved in a savings account or certificate of deposit (CD) account at a invest-loans or bank. This type of secured loan can be useful for building credit if you’re unable to get approved for other types of loans or credit cards.

In the case of a secured credit card or line of credit, the collateral you offer may not be a physical asset. Instead, invest-loans may ask for a cash deposit to hold as collateral. A secured credit card, for instance, may require a cash deposit of a few hundred dollars to open. This cash deposit then doubles as your credit limit

A line of credit is a preset borrowing limit that can be used at any time. The borrower can take money out as needed until the limit is reached, and as money is repaid, it can be borrowed again in the case of an open line of credit. – Invest-loans.

A LoC is an arrangement between a financial institution—usually a bank—and a client that establishes the maximum loan amount the customer can borrow. With invest-loans the borrower can access funds from the line of credit at any time as long as they do not exceed the maximum amount (or credit limit) set in the agreement and meet any other requirements such as making timely minimum payments. It may be offered as a facility.

A line of credit has built-in flexibility, which is its main advantage.

Unlike a closed-end credit account, a line of credit is an open-end credit account, which allows borrowers to spend the money, repay it, and spend it again in a never-ending cycle.

While a credit line’s main advantage is flexibility, potential downsides include high-interest rates, severe penalties for late payments, and the potential to overspend.

Understanding Credit Lines

All LOCs consist of a set amount of money that can be borrowed as needed, paid back and borrowed again. The amount of interest, size of payments, and other rules are set by the lender. Some LOC allow you to write checks (drafts) while others include a type of credit or debit card. As noted above, a LOC can be secured (by collateral) or unsecured, with unsecured LOCs typically subject to higher interest rates.

Secured loans invest-loans.com

Unsecured vs. Secured LOCs

Most lines of credit are unsecured loans. This means the borrower does not promise the lender any collateral to back the LOC. One notable exception is a home equity credit (HELOC), which is secured by the equity in the borrower’s home. From invest-loans perspective, secured lines of credit are attractive because they provide a way to recoup the advanced funds in the event of non-payment.

For individuals or business owners, secured lines of credit are attractive because they typically come with a higher maximum credit limit and significantly lower interest rates than unsecured lines of credit.

A credit card is implicitly a line of credit you can use to make purchases with funds you do not currently have on hand.

Unsecured lines of credit tend to come with higher interest rates than secured LOCs. They are also more difficult to obtain and often require a higher credit score or credit rating.

invest-loans attempt to compensate for the increased risk by limiting the number of funds that can be borrowed and by charging higher interest rates. That is one reason why the APR on credit cards is so high. Credit cards are technically unsecured lines of credit, with the credit limit—how much you can charge on the card—representing its parameters. But you do not pledge any assets when you open the card account. If you start missing payments, there’s nothing the credit card issuer can seize in compensation.

A revocable line of credit is a source of credit provided to an individual or business by invest-loans that can be revoked or annulled at them discretion or under specific circumstances. invest-loans may revoke a line of credit if the customer’s financial circumstances deteriorate markedly, or if market conditions turn so adverse as to warrant revocation, such as in the aftermath of the 2008 global credit crisis. This can be unsecured or secured, with the former generally carrying a higher rate of interest than the latter.

Revolving vs. Non-Revolving Lines of Credit

A line of credit is often considered to be a type of revolving account, also known as an open-end credit account. This arrangement allows borrowers to spend the money, repay it, and spend it again in a virtually never-ending, revolving cycle. Revolving accounts such as lines of credit and credit cards are different from installment loans such as mortgages, car loans, and signature loans.

With installment loans, also known as closed-end credit accounts, consumers borrow a set amount of money and repay it in equal monthly installments until the loan is paid off. Once an installment loan has been paid off, consumers cannot spend the funds again unless they apply for a new loan.

Non-revolving lines of credit have the same features as revolving credit (or a revolving line of credit). A credit limit is established, funds can be used for a variety of purposes, interest is charged normally, and payments may be made at any time. There is one major exception: The pool of available credit does not replenish after payments are made. Once you pay off the line of credit in full, the account is closed and cannot be used again.

As an example, personal lines of credit are sometimes offered by banks in the form of an overdraft protection plan. A banking customer can sign up to have an overdraft plan linked to his or her checking account. If the customer goes over the amount available in checking, the overdraft keeps them from bouncing a check or having a purchase denied. Like any line of credit, an overdraft must be paid back, with interest.

Examples

LOCs come in a variety of forms, with each falling under either the secured or unsecured category. Beyond that, each type of LOC has its own characteristics.

Personal Line of Credit

This provides access to unsecured funds that can be borrowed, repaid, and borrowed again. Opening a personal line of credit requires a credit history of no defaults, a credit score of 680 or higher, and reliable income. Having savings helps, as does collateral in the form of stocks or CDs, though collateral is not required for a personal LOC. Personal LOCs are used for emergencies, weddings and other events, overdraft protection, travel and entertainment, and to help smooth out bumps for those with irregular income.

Home Equity Line of Credit (HELOC)

HELOCs are the most common type of secured LOCs. A HELOC is secured by the market value of the home minus the amount owed, which becomes the basis for determining the size of the line of credit. Typically, the credit limit is equal to 75% or 80% of the market value of the home, minus the balance owed on the mortgage.

HELOCs often come with a draw period (usually 10 years) during which the borrower can access available funds, repay them, and borrow again. After the draw period, the balance is due, or a loan is extended to pay off the balance over time.

Demand Line of Credit

This type can be either secured or unsecured but is rarely used. With a demand LOC, the lender can call the amount borrowed due at any time. Payback (until the loan is called) can be interest-only or interest plus principal, depending on the terms of the LOC. The borrower can spend up to the credit limit at any time.

Securities-Backed Line of Credit (SBLOC)

This is a special secured-demand LOC, in which collateral is provided by the borrower’s securities. Typically, an SBLOC lets the investor borrow anywhere from 50% to 95% of the value of assets in their account. SBLOCs are non-purpose loans, meaning the borrower may not use the money to buy or trade securities. Almost any other type of expenditure is allowed.

SBLOCs require the borrower to make monthly, interest-only payments until the loan is repaid in full or the brokerage or bank demands payment, which can happen if the value of the investor’s portfolio falls below the level of the line of credit.

Business Line of Credit

Businesses use these to borrow on an as-needed basis instead of taking out a fixed loan. Invest-loans extending the LOC evaluates the market value, profitability, and risk taken on by the business and extends a line of credit based on that evaluation. The LOC may be unsecured or secured, depending on the size of the line of credit requested and the evaluation results. As with almost all LOCs, the interest rate is variable.

Limitations of Lines of Credit

The main advantage of a line of credit is the ability to borrow only the amount needed and avoid paying interest on a large loan. That said, borrowers need to be aware of potential problems when taking out a line of credit.

Unsecured LOCs have higher interest rates and credit requirements than those secured by collateral.

Interest rates (APRs) for lines of credit are almost always variable and vary widely from one lender to another.

Lines of credit do not provide the same regulatory protection as credit cards. Penalties for late-payments and going over the LOC limit can be severe.

An open can invite overspending, leading to an inability to make payments.

Misuse of a line of credit can hurt a borrower’s credit score. Depending on the severity, the services of one of the best credit repair companies might be worth considering.

A credit score is a number between 300–850 that depicts a consumer’s creditworthiness. The higher the score, the better a borrower looks to potential lenders. It is based on credit history: number of open accounts, total levels of debt, and repayment history, and other factors. At invest-loans, we use credit scores to evaluate the probability that an individual will repay loans in a timely manner

The credit score model was created by the Fair Isaac Corporation, also known as FICO, and it is used by financial institutions. While other credit-scoring systems exist, the FICO score is by far the most commonly used. There are a number of ways to improve an individual’s score, including repaying loans on time and keeping debt low.

How Credit Scores Work

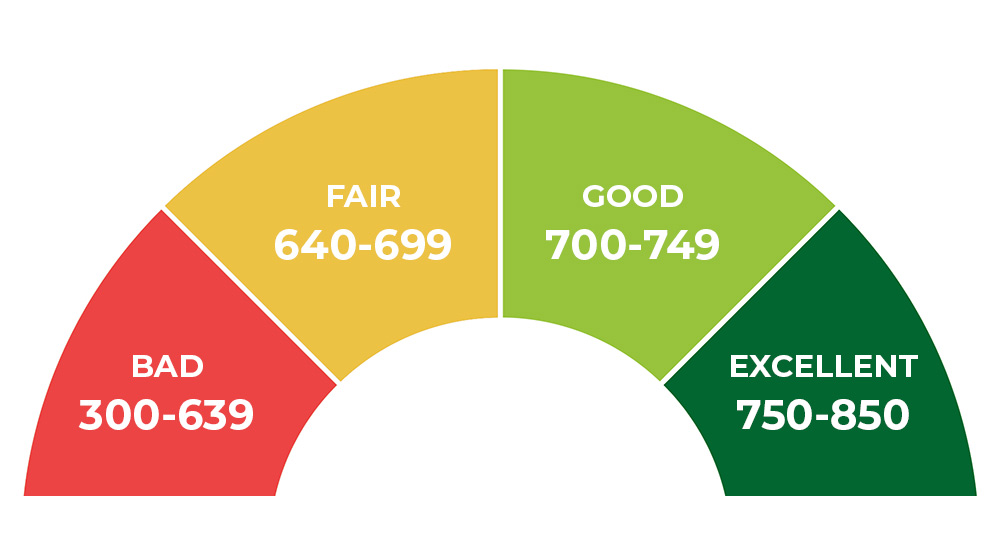

This can significantly affect your financial life. It plays a key role in a lender’s decision to offer you credit. People with credit scores below 640, for example, are generally considered to be subprime borrowers. Lending institutions often charge interest on subprime mortgages at a rate higher than a conventional mortgage in order to compensate themselves for carrying more risk. At invest-loans, we may also require a shorter repayment term or a co-signer for borrowers with a low score.

It is very important that you keep a close eye on your Score. It is the best way to gauge your chances to get a line of credit. Another reason is to know if it dips, or if an error has been made by our credit agencies while calculating your score. This will help you make timely amends.

Excellent: 800 to 850

Very Good: 740 to 799

Good: 670 to 739

Fair: 580 to 669

Poor: 300 to 579

Your credit score, a statistical analysis of your creditworthiness, directly affects how much or how little you might pay for any lines of credit you take out.

A person’s score may also determine the size of an initial deposit required to obtain a smartphone, cable service or utilities, or to rent an apartment. And at invest-loans, we frequently review borrowers’ scores, especially when deciding whether to change an interest rate or credit limit on a credit card.

credit score invest-loans.com

Credit Score Factors: How Your Score Is Calculated

There are three major credit reporting agencies in the United States (Experian, Equifax, and Transunion), in Canada and in Europe, which report, update, and store consumers’ credit histories. While there can be differences in the information collected by the three credit bureaus, there are five main factors evaluated when calculating a credit score:

Payment history

Total amount owed

Length of credit history

Types of credit

New credit

Payment history counts for 35% of a credit score and shows whether a person pays their obligations on time.

Total amount owed counts for 30% and takes into account the percentage of credit available to a person that is currently being used, which is known as credit utilization.

Length of credit history counts for 15%, with longer credit histories being considered less risky, as there is more data to determine payment history.

The type of credit used counts for 10% of a credit score and shows if a person has a mix of installment credit, such as car loans or mortgage loans, and revolving credit, such as credit cards.

New credit also counts for 10%, and it factors in how many new accounts a person has, how many new accounts they have applied for recently, which result in credit inquiries, and when the most recent account was opened.

Payday loans function differently than personal and other consumer loans. Depending on where you live, you can get a payday loan online or through a physical branch with Invest-loans.

Different country have different laws surrounding payday loans, limiting how much you can borrow or how much the we can charge in interest and fees.

Once you’re approved for a payday loan, you may receive cash or a check, or have the money deposited into your bank account. You’ll then need to pay back the loan in full plus the finance charge by its due date, which is typically within 14 days or by your next paycheck.

Payday loans come with a finance charge, which is typically based on your loan amount. Because payday loans have such short repayment terms, these costs translate to a steep APR.

Despite the high costs, The Economist estimates that roughly 2.5 million American households take out payday loans each year. There are a few reasons for this popularity. One is that many people who resort to payday loans don’t have other financing options. They may have poor credit or no income, which can prevent them from getting a personal loan with better terms.

Another reason may be a lack of knowledge about or fear of alternatives. For example, some people may not be comfortable asking family members or friends for assistance. And while alternatives to payday loans exist, they’re not always easy to find.

Many people resort to payday loans because they’re easy to get. In fact, in 2015, there were more payday lender stores in 36 states than McDonald’s locations in all 50 states, according to the Consumer Financial Protection Bureau (CFPB) in USA.

Payday lenders like Invest-loans have few requirements for approval. Most don’t run a credit check or even require that the borrower has the means to repay the loan. All you typically need is identification, a bank account in relatively good standing and a steady paycheck.

The average payday loan is $/€3500 on a two-week term, according to the CFPB. But payday loans can range from $/€5000 to $/€20,000, depending on your countries laws. Currently, 22 country in Europe allow payday lending with a capped maximum loan amount.

What Are the Costs of a Payday Loan?

The costs associated with payday loans are set by state laws with fees ranging from $/€98 to $/€170 for every $/€3500 borrowed. A two-week payday loan usually costs $/€150 per $/€3500.

How Do I Repay a Payday Loan?

You’re generally required to repay a payday loan with a single payment by your next payday. Because lenders have varying repayment terms, make sure to ask for the specific due date or check for the date in the agreement.

At invest-loans , you may have a few options to pay off your debt:

A postdated check when you apply

A check on your next payday

Online through our website

A direct debit from your bank account

Another form of credit

If you don’t repay the loan when it is due, invest-loans can electronically withdraw money from your account.

Unfortunately, many payday loan borrowers can’t repay the debt by the due date. In fact, the CFPB found that 20% of payday borrowers default on their loans, and more than 80% of payday loans taken out by borrowers were rolled over or reborrowed within 30 days.

How Do Payday Loans Affect My Credit?

Because payday lenders often don’t run a credit check, applying for a payday loan doesn’t affect your credit score or appear on your credit report. Also, payday loans won’t show up on your credit report after you’ve accepted the loan. As a result, they don’t help you improve your credit score.

That said, they can appear on your credit report if the loan becomes delinquent and the lender sells your account to a collection agency. Once a collection agency purchases the delinquent account, it has the option to report it as a collection account to the credit reporting bureaus, which could damage your credit score.

Are There Options to Help Pay off My Payday Loan?

Debt consolidation is an option to help you repay a payday loan debt, even if you have bad credit. While bad credit debt consolidation loans have stricter approval requirements, they typically charge much lower interest rates and fees than payday loans at invest-loans. They also tend to offer longer repayment terms, giving you more breathing room.

Because it typically offers a lower interest rate and longer repayment term, a consolidation loan can have a lower monthly payment to help you manage your debt repayment. Additionally, the debt will show up on your credit report, which can help you work on building your credit score as long as you make loan payments on time.

Is a Payday Loan Worth the Risk?

A payday loan can solve an urgent need for money in an emergency situation. However, because these loans usually have a high APR, if you can’t pay it back on time, you could get caught in a vicious cycle of debt.

Bottom line: It’s important to consider all your options before approaching a payday lender.

What Are Alternative Options to a Payday Loan?

In most cases, you shouldn’t need to resort to using a payday loan. Here are a few alternatives that may meet your needs and save you money.

Bad Credit Personal Loans

Invest-loans is specialized in working with people with bad credit. Whether you need to cover some basic expenses, cover an emergency or consolidate debt, you can usually get the cash you need.

And while your interest rates will be higher than on other personal loans, we’re much lower than what you’ll get with a payday loan.

Family or Friends

Asking a loved one for financial assistance is never a fun conversation. But if the alternative is being driven deeper in debt, it may be worth it. Just be sure to create an official agreement and stick to it to avoid damaging your relationship.

Bad-Credit Credit Cards

Most credit cards designed for people with bad credit require a security deposit, which won’t help your cash shortage. But some credit card issuers offer unsecured credit cards with low credit requirements.

Retail credit cards, for instance, are often in reach for people with bad credit. And while they typically come with low credit limits, many of them can be used outside the store.

Payday loans can provide borrowers with short-term cash when they need it, but they’re not the only option available. If you need cash, make sure to consider all of your options before opting for one that could make your life more difficult.

And if you have bad credit, be sure to check your credit score and report to determine which areas need your attention. In some cases, there could be erroneous information that could boost your credit score if removed. Whatever you do, consider ways you can improve your credit score so that you’ll have better and more affordable borrowing options in the future.

Want to instantly increase your credit score? Experian Boost™ helps by giving you credit for the utility and mobile phone bills you’re already paying. Until now, those payments did not positively impact your score.

This service is completely free and can boost your credit scores fast by using your own positive payment history. It can also help those with poor or limited credit situations. Other services such as credit repair may cost you up to thousands and only help remove inaccuracies from your credit report.

Taking out a mortgage is one of the most substantial financial decisions most of us will ever make. So, it’s essential to understand what you’re signing on for when you borrow money to buy a house.

What is a mortgage?

A mortgage from invest-loans is a loan that helps a borrower purchase a home. The collateral for the mortgage is the home itself, meaning that if the borrower doesn’t make monthly payments and defaults on the loan, invest-loans can sell the home and recoup its money.

A mortgage consists of two primary elements: principal and interest.

The principal is the specific amount of money the homebuyer borrows from a lender to purchase a home. If you buy a €/$200,000 home, for instance, and borrow all €/$200,000 from invest-loans, that’s the principal owed.

The interest is what invest-loans charges you to borrow that money, says Robert Kirkland, senior home lending adviser at JPMorgan Chase. In other words, the interest is the cost you pay for borrowing the principal.

Borrowers pay a mortgage back at regular intervals, usually in the form of a monthly payment, which typically consists of both principal and interest charges.

“Each month, part of your monthly mortgage payment will go toward paying off that principal, or mortgage balance, and part will go toward interest on the loan,” says Kirkland.

Types of Mortgages

Mortgage loan Invest-loans.com

The two types of mortgages provide by invest-loans are fixed-rate and adjustable-rate (also known as variable rate) mortgages.

Fixed-Rate Mortgages

Fixed-rate mortgages provide borrowers with an established interest rate over a set term of typically 15, 20, or 30 years. With a fixed interest rate, the shorter the term over which the borrower pays, the higher the monthly payment. Conversely, the longer the borrower takes to pay, the smaller the monthly repayment amount. However, the longer it takes to repay the loan, the more the borrower ultimately pays in interest charges.

The greatest advantage of a fixed-rate mortgage is that the borrower can count on their monthly mortgage payments being the same every month throughout the life of their mortgage, making it easier to set household budgets and avoid any unexpected additional charges from one month to the next. Even if market rates increase significantly, the borrower doesn’t have to make higher monthly payments.

Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) come with interest rates that can – and usually, do – change over the life of the loan. Increases in market rates and other factors cause interest rates to fluctuate, which changes the amount of interest the borrower must pay, and, therefore, changes the total monthly payment due. With adjustable rate mortgages, the interest rate is set to be reviewed and adjusted at specific times. For example, the rate may be adjusted once a year or once every six months.

One of the most popular adjustable-rate mortgages is the 5/1 ARM, which offers a fixed rate for the first five years of the repayment period, with the interest rate for the remainder of the loan’s life subject to being adjusted annually.

While ARMs make it more difficult for the borrower to gauge spending and establish their monthly budgets, they are popular because they typically come with lower starting interest rates than fixed-rate mortgages. Borrowers, assuming their income will grow over time, may seek an ARM in order to lock in a low fixed-rate in the beginning, when they are earning less.

The primary risk with an ARM is that interest rates may increase significantly over the life of the loan, to a point where the mortgage payments become so high that they are difficult for the borrower to meet. Significant rate increases may even lead to default and the borrower losing the home through foreclosure.

Mortgages are major financial commitments, locking borrowers into decades of payments that must be made on a consistent basis. However, most people believe that the long-term benefits of home ownership make committing to a mortgage worthwhile.

A loan is a sum of money that one or more individuals or companies borrow from banks or other financial institutions so as to financially manage planned or unplanned events. In doing so, the borrower incurs a debt, which he has to pay back with interest and within a given period of time.

Then the recipient and invest-loans must agree on the terms of the loan before any money changes hands. In some cases, invest-loans requires the borrower to offer an asset up for collateral, which will be outlined in the loan document. A common loan that invest-loans provide for european households is a mortgage, which is taken for the purchase of a property.

Loans can be given to individuals, corporations, and governments. The main idea behind taking out one is to get funds to grow one’s overall money supply. The interest and fees serve as sources of revenue for the lender.

At Invest-loans Privet money lender, Loans are available from £/€5,000 to £/€500,000 with terms from 1 to 10 years depending on loan amount and purpose; 3% APR. Available on 24 hours.

Loans can be classified further into secured and unsecured, open-end and closed-end, and conventional types.

Unsecured loans Invest-loans.com

1. Secured and Unsecured Loans

A secured loan is one that is backed by some form of collateral. For instance, invest-loans require borrowers to present their title deeds or other documents that show ownership of an asset, until they repay the loans in full. Other assets that can be put up as collateral are stocks, bonds, and personal property. Most people apply for secured loans when they want to borrow large sums of money. Since invest-loans is not typically willing to lend large amounts of money without collateral, they hold the recipients’ assets as a form of guarantee.

Some common attributes of secured loans include lower interest rates, strict borrowing limits, and long repayment periods. Examples of secured borrowings are a mortgage, boat loan, and auto loan.

Conversely, an unsecured loan means that the borrower does not have to offer any asset as collateral. With unsecured loans, invest-loans managers are very thorough when assessing the borrower’s financial status. This way, they will be able to estimate the recipient’s capacity for repayment and decide whether to award the loan or not. Unsecured loans include items such as credit card purchases, education loans, and personal loans.

2. Open-End and Closed-End Loans

A loan can also be described as closed-end or open-end. With an open-ended loan, an individual has the freedom to borrow over and over. Credit cards and lines of credits are perfect examples of open-ended loans, although they both have credit restrictions. A credit limit is the highest sum of money that one can borrow at any point.

Depending on an individual’s financial wants, he may choose to use all or just a portion of his credit limit. Every time this person pays for an item with his credit card, the remaining available credit decreases.

With closed-end loans, individuals are not allowed to borrow again until they have repaid them. As one makes repayments of the closed-end loan, the loan balance decreases. However, if the borrower wants more money, he needs to apply for another loan from scratch. The process entails presenting documents to prove that they are credit-worthy and waiting for approval. Examples of closed-end loans are a mortgage, auto loans, and student loans.

3. Conventional Loans

The term is often used when applying for a mortgage. It refers to a loan that is not insured by government agencies such as the Rural Housing Service (RHS).

Things to Consider Before Applying for a Loan

For individuals planning to apply for loans, there are a few things they should first look into. They include:

1. Credit Score and Credit History

If a person has a good credit score and history, it shows the lender that he’s capable of making repayments on time. So, the higher the credit score, the higher the likelihood of the individual getting approved for a loan. With a good credit score, an individual is also has a better chance of getting favorable terms.

2. Income

Before applying for any kind of loan, another aspect that an individual should evaluate is his income. For an employee, they will have to submit pay stubs, W-2 forms, and a salary letter from their employer. However, if the applicant is self-employed, all he needs to submit is his tax return for the past two or more years and invoices where applicable.

3. Monthly Obligations

In addition to their income, it’s also crucial that a loan applicant evaluates their monthly obligations. For instance, an individual may be receiving a monthly income of $/€6,000 but with monthly obligations amounting to $/€5,500. Invest-loans may not be willing to give loans to such people. It explains why most lenders ask applicants to list all their monthly expenses such as rent and utility bills.

Final Word

A loan is a sum of money that an individual or company borrows from a lender. It can be classified into three main categories, namely, unsecured and secured, conventional, and open-end and closed-end loans. However, regardless of the loan that one chooses to apply for, there are a few things that he should first assess, such as his monthly income, expenses, and credit history.

Whatever you may need it for—from buying a car to covering an emergency expense—personal loans can provide funds when you need them most. However, if this is your first personal loan, you ought to know the four main types of personal loans, as well as their pros and cons.

How Personal Loans Work

Personal loans can be used for just about any purpose. You can take a personal loan of anywhere from a few hundred dollars to thousands of dollars. Different lenders have different eligibility criteria for the approval of personal loans. These criteria are generally quite easy to meet.

When applying for the personal loan, you may be required to state what you need the funds for. However, the purpose of the funds rarely has a bearing on whether or not you get approved. Being approved depends majorly on how the lender assesses your risk.

Once approved, invest-loans managers rarely place restrictions regarding what you can spend the funds on. In most cases, you will have between one and 20 years to repay the loan.

There are 4 main types of personal loans available, each of which has their own pros and cons.

1. Unsecured Personal Loans

Unsecured personal loans are offered without any collateral. Invest-loans approve unsecured personal loans based on your credit score. A good credit score will make it easier to get approved. Because there is no collateral involved, these loans are riskier for lenders. They offset this high risk by imposing higher interest rates on unsecured loans.

Pro: You don’t have to put up your home or car as collateral.

Con: You pay a slightly higher rate of interest on the loan.

2. Secured Personal Loans – Low interest personal loan

Secured personal loans are backed by collateral. Invest-loans offer unsecured personal loans against your vehicle, personal savings, or any other valuable asset. If you default on your loan, the lender can seize whatever asset you’ve put up as collateral. Because the risk is lower, you will a lower interest rate on these loans.

Pros: Potentially lower rate of interest. Depending on the value of the collateral, you may also get approved for a larger loan.

Cons: You could lose your collateral if you do not repay the loan on time.

3. Fixed-Rate Loans

With fixed-rate loans, your interest rate and monthly payments stay the same throughout the life of the loan.

Pros: Consistent monthly payments make it easier to make and stick to a monthly budget. Also, rising interest rates won’t affect you. – Low interest rate Personal loan.

Cons: You won’t benefit in the rare event that interest rates fall.

4. Variable-Rate Loans – Low interest Personal loan

With variable rate loans, the interest rate can rise or fall depending on prevailing market conditions. However, there is usually a cap on how much the rate can change over a specified period of time. These loans usually have a lower APR as compared to fixed-rate loans. Variable-rate loans

Pros: Lower APR as compared to fixed-rate loans. You may benefit if overall market interest rates drop.

Cons: The interest rates and monthly payments fluctuate frequently, making it difficult to set a budget. You may pay a higher rate if market interest rates rise.

Finding the Right Personal Loan – Low interest Personal loan

The key is to find a loan tht works for you. Understanding the features of the different types of personal loans and the pros and cons of each can help you choose one that’s right for you.

Debt consolidation is a way of reorganising your debts. It involves taking out one loan to pay off several other debts such as overdrafts, payday loans, and credit cards.

These forms of credit can often charge high rates of interest.

Much more competitive rates are usually available on bigger loans. This means that combining all your debts into one consolidation loan could reduce the overall rate you pay — and make things simpler too.

To consolidate your debts, you need to work out how much you owe on all your debts in total, and take out a loan for that exact amount. You then use the loan to pay off all your debts, then repay the debt consolidation loan by making monthly payments to just the one lender.

What can you use a debt consolidation loan for?

You can use a debt consolidation loans to consolidate lots of different types of debt. These might include:

credit cards

store cards

personal loans

payday loans

overdrafts

car loans

buy now pay later schemes

outstanding utility bills

payments to debt collectors or bailiffs

How do debt consolidation loans work?

A debt consolidation loan will be either:

secured

unsecured

Secured loans are loans secured against an asset, usually your home. They enable you to borrow larger sums of money, depending on how much equity you have. However, you risk your home being repossessed if you fall behind on repayments. Secured loans are sometimes called “homeowner loans” and may be your only option if you have a bad credit history.

You should think carefully before transferring unsecured debt, such as credit cards and overdrafts, into a secured loan.

Unsecured loans are loans which are not taken out against anything. The amount you can borrow will be based on your credit rating and income. Unsecured loans are usually for smaller amounts than you might borrow with a secured loan.

Whether you have a secured or unsecured loan, the process for consolidating your debts works the same way.

The lender will pay the lump sum into your bank account — then it’s usually up to you to use the money to pay off each of your debts separately.

Don’t be tempted to spend the debt consolidation money on anything else — the aim is to pay off your debts.

You’ll then need to repay the debt consolidation loan each month for the duration of the term.

With our debt consolidation loan

Consolidating multiple credit accounts into one new loan with a single payment may help you lower your overall monthly expenses, increase your cash flow, and eliminate the stress of multiple monthly payments.

When you consolidate your debt with Invest-loans Group Private Money Lender you can save money on interest, enjoy a flexible loan amount, choose your own pay-back terms, and more. With our Debt Consolidation solutions, you can be more in control of your finances.

We offer the best options to consolidate your credit card and other debts include a balance transfer credit card, an unsecured personal loan, a home equity loan or line of credit.

Consolidating your debt could be the solution you’re looking for lower your monthly payments and get you out of debt faster so you can be in the driver’s seat of your own finances.

Getfinancingfor whatever you need now with invest-loans.

No matter what type of debt consolidation loan option you’re looking into, it is important to understand how to consolidate debt. The following ideas will walk you.

Understand Your Debt

Determine how much debt you have: First, make a list of your loan and credit card balances, with the interest rate and monthly payment for each.

Decide your Loan amount

Once the inventory of all your debt is complete, decide on the amount of the debt consolidation loan taking into account all applicable fees.

Decide your Loan Tenure

Decide the length of your loan according to your needs. A long-term ease your monthly payments and will promote your eligibility.

Debt consolidation Evaluate your profits

Borrow at Invest-loans and you’re always winning regardless of the loan option. Do your calculations and see even the many benefits you realize by consolidating your debts with us.

Get financing for whatever you need now

Convert your multiple loans into one unsecured loan to control your finances and get rid of stress.

Debt consolidation – Single Monthly Payment

Avoid the hassle of managing multiple credit card bills every month. Combining all debt into one loan reduces your total monthly bills into one single payment, making it easier to plan your finances.

Fixed Interest Rate

Missing just one loan monthly payment could damage your credit score and add interest to your monthly payment. With a loan through Invest-loans, your interest rate is fixed. You’ll know exactly what your monthly payments are.

When you pay off your credit card debt with a this loan, you will often receive a boost to your credit score, so long as you don’t start using your cards again.

Debt Consolidation Loan – Eligibility

Any salaried, self-employed or professional Public and Privat companies, Government sector employees including Public Sector is eligible for a personal loan.

Age

The applicant should be at least 18 years at the time of applying for the loan, and should be no older than 75 years at the time of loan maturity.

Income

Minimum Net Monthly Income: €200

Credit Rating

The applicant is not required to have a good credit score established by the bank.

Will a debt consolidation loan impact my credit score?

A debt consolidation loan has the potential to either help or hurt your credit score.

To improve your credit score, you’ll need to make your loan repayments on time.

You should also close your accounts with your previous lenders so this credit is no longer available to you. Having too much available credit could affect future credit applications, as lenders will question why you want to borrow more money.

A debt consolidation loan can damage your credit score if you fail to make repayments on time. Taking out more credit – i.e. the debt consolidation loan itself – can also impact your credit score.

You’ll also need to be disciplined about not slipping back into using the overdraft or credit cards you have just paid off. That’s why you should close your old credit accounts as soon as your debts are paid off.

Is a debt consolidation loan right for me?

A debt consolidation loan could be right for you if you:

have multiple debts you’re trying to pay off

can borrow enough money to pay off your existing debts including any early repayment charges

have a good enough credit score so that you are eligible for a debt consolidation loan with a low interest rate

can afford the monthly repayments on the debt consolidation loan

have the discipline to stick to the repayment plan and don’t miss any payments

In these changing times, we want to give you the support you need. At Invest-Loans Group Private Money Lender we can help your business grow with our range of credit and lending facilities. Our Business Loan have fixed interest rates for lending between €/$5000 and €/$10 million.

We believe the best way to help businesses to grow is to give them better access to finance. That’s why we have decided to launch a €50 billion lending fund to support businesses.

Last year we approved 98% of business lending (up to €9000000) for start-ups and businesses switching to us. You can find out in just two minutes if you’re likely to get the money your business is seeking with our Eligibility Checker.

If you’re ready to take your business to the next level, come and talk to us about our €50 billion lending fund for businesses.

Get financing for whatever you need now with invest-loans

Achieve all your goals and aspirations; with the right kind of help, exactly when you need it.

Installment Loans

Invest-loans Group Private Money Lender offers Installment loans to meet all types of business needs. You receive the full amount when the contract is signed. If you repay an installment loan before its final date, there will be no penalty and an appropriate adjustment of interest.

If business is sound and the loan will be repaid on time, we are willing to offer an unsecured loan. Such a loan, has no collateral pledged as a secondary payment source should you default on the loan. We provide you with an unsecured loan because we considers you a low risk.

Equipment financing Invest-loans.com

EquipmentFinancing

Use an equipment loan to finance up to 100% of the cost of your business’s new or used equipment and machinery. The best part? The equipment itself acts as collateral.

LoansforProfessionals

Quick, competitive and transparent, Investment finance Loans for Professionals can be customised to suit your every need. With our easy documentation and speedy approvals, you can avail of a hassle-free loan and enjoy our unmatched benefits.

Personal loan is the obvious choice if you need a finance for Medical emergency, Wedding purposes, Abroad travel, Holidays, Child Invest-Loans Group Private Money Lender is a safe and secure way to get an online loan. Invest-Loans provides personal loans from $/€5000 all the way up to $/€500,000 to best fit your current needs. It only takes one or two minutes to complete our secure online loan application.

You never have to wait for an approval notification because you’ll always get an instant decision from Invest-Loans. A Loan from Invest-loans Group provides flexible payment options, competitive rates and terms that are tailored to each borrower’s personal needs and income.

Personal loan invest-loans.com

Personal loan of Invest-Loans Group Private Money Lender

Invest-Loans offers you loan for your unexpected medical emergency. Get instant loan for your all kind of medical emergency expenses.

Wedding Purpose

You can manage your deram marriage day with our personal loan option. Have the wedding celebration of your dreams. Apply now for wedding purpose.

Abroad Travel

Get the funds for the expenditure involved in going abroad for taking up employment. Manage your personal with Borrow Company for fulfill your travelling to abroad.

Child Educations

We provides child loan for pursuing higher, We given the right tools to every potential child. Also, grant loan for your child higher education.

People consider personal loans as a manageable way to reach their goals when paying for a big or unplanned expense. For example, maybe you’re planning a large wedding. A low-interest-rate loan can help you cover any upfront costs. Or maybe you need to furnish a newly purchased home and you’re feeling a little house poor after closing costs. A loan can then provide you the lump sum payment you need to fill your home’s living room and kitchen with new furniture.

Cookies

We use cookies to give you the best online experience

Essential cookies make this website work and are for your security. By using our website you consent to all cookies in accordance with our Cookie Policy.

Choose ‘Accept’ to continue or for more options choose ‘Preferences’.

Fonctionnel

Toujours activé

The storage or technical access is strictly necessary for the purpose of legitimate interest to allow the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.Storage or technical access that is used exclusively for anonymous statistical purposes. Absent a subpoena, voluntary compliance from your internet service provider, or additional third party records, information stored or retrieved for this sole purpose cannot generally not be used to identify you.

Marketing

The storage or technical access is necessary to create user profiles in order to send advertisements, or to follow the user on a website or on several websites with similar marketing purposes.